Page 311 - Bank Muamalat_AR24

P. 311

ANNUAL REPORT 2024 1 2 3 4 5 6 7 Our Numbers 8 309

47. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES (CONT’D.)

(a) Credit risk (cont’d.)

(ii) Credit quality for financing of customers (cont’d.)

Past due but not impaired (cont’d.)

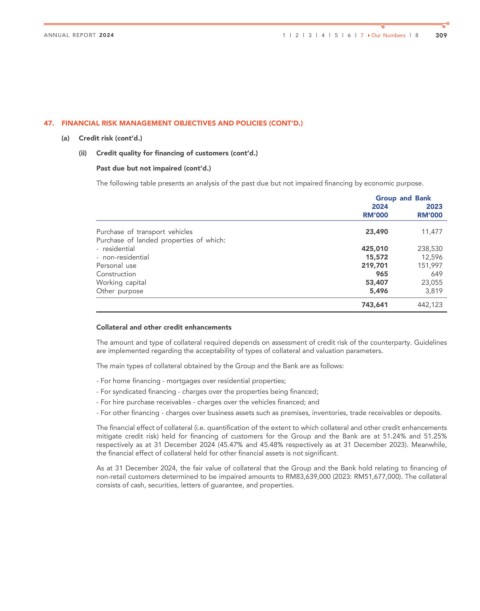

The following table presents an analysis of the past due but not impaired financing by economic purpose.

Group and Bank

2024 2023

RM’000 RM’000

Purchase of transport vehicles 23,490 11,477

Purchase of landed properties of which:

- residential 425,010 238,530

- non-residential 15,572 12,596

Personal use 219,701 151,997

Construction 965 649

Working capital 53,407 23,055

Other purpose 5,496 3,819

743,641 442,123

Collateral and other credit enhancements

The amount and type of collateral required depends on assessment of credit risk of the counterparty. Guidelines

are implemented regarding the acceptability of types of collateral and valuation parameters.

The main types of collateral obtained by the Group and the Bank are as follows:

- For home financing - mortgages over residential properties;

- For syndicated financing - charges over the properties being financed;

- For hire purchase receivables - charges over the vehicles financed; and

- For other financing - charges over business assets such as premises, inventories, trade receivables or deposits.

The financial effect of collateral (i.e. quantification of the extent to which collateral and other credit enhancements

mitigate credit risk) held for financing of customers for the Group and the Bank are at 51.24% and 51.25%

respectively as at 31 December 2024 (45.47% and 45.48% respectively as at 31 December 2023). Meanwhile,

the financial effect of collateral held for other financial assets is not significant.

As at 31 December 2024, the fair value of collateral that the Group and the Bank hold relating to financing of

non-retail customers determined to be impaired amounts to RM83,639,000 (2023: RM51,677,000). The collateral

consists of cash, securities, letters of guarantee, and properties.